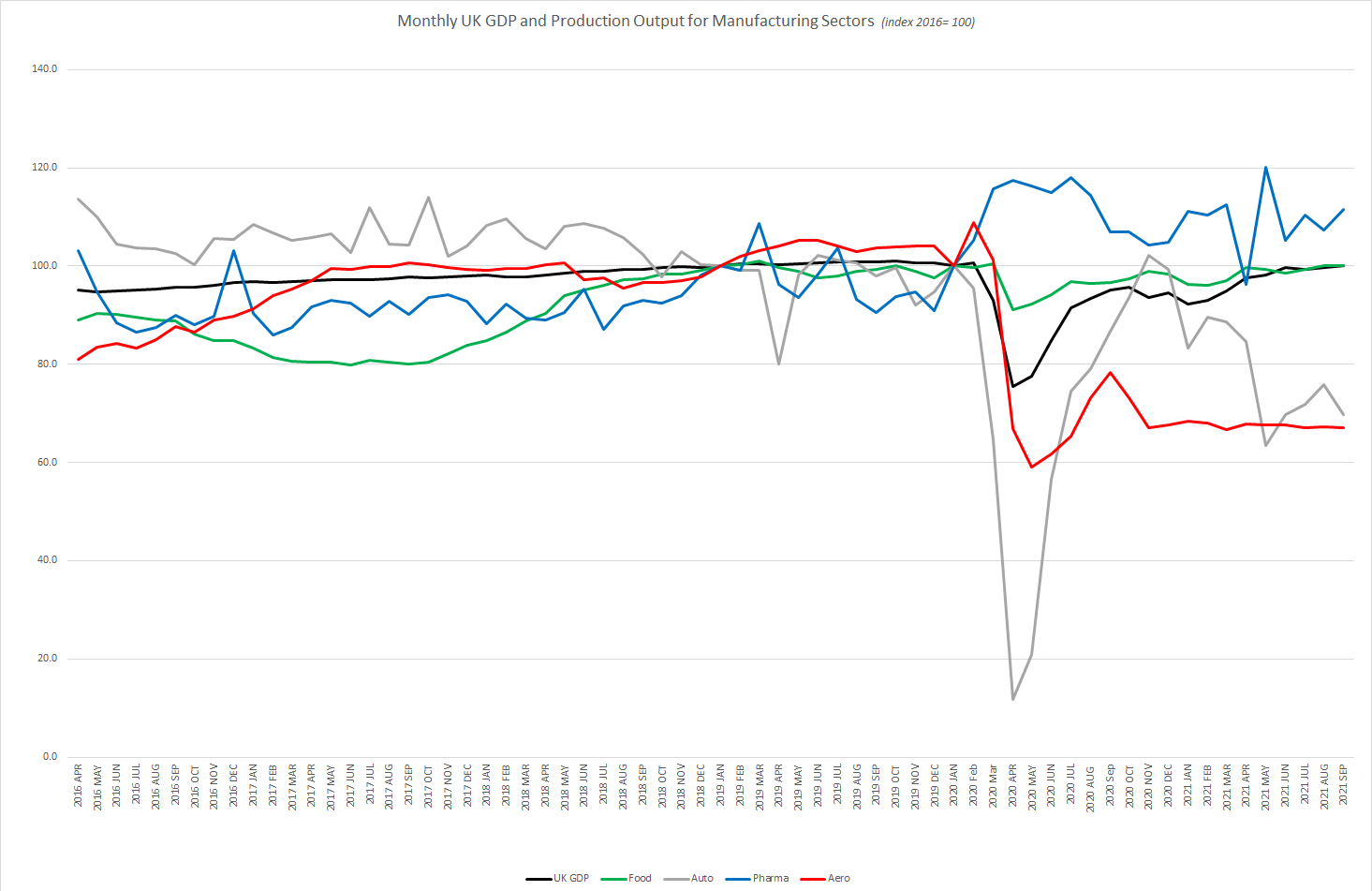

This week’s GDP figures give us a first look at the economic recovery in the month of September and also the third quarter of 2021. As suspected supply chain disruption is blamed for slower growth despite a reopened economy. Shortage of some products, raw materials, ongoing disruption from Brexit and COVID and a shortage of hauliers means that the supply chain has literally not been able to cope with the increased global demand.

Less than one percent UK GDP monthly growth in September 2021, couple with revised down growth in July sets the growth expectations for the year back slightly. However, at September GDP is just 0.6% behind where it was pre-pandemic (February 2020) and is 5.3% ahead of the same month in 2020 when more restrictions were in place.

UK GDP grew by 1.3% in Q3 2021 at first estimates, this is a significant slowing from the 5.2% growth in Q2 2021. Both services and production output both grew in the quarter by 1.6% and 0.8% respectfully with services supporting the majority of growth. Production output remains 1.4% below pre-pandemic levels (February 2020) and the month of September actually saw a decrease in output of 0.4% as the resumption of services led economic recovery.

Manufacturing Production declines amidst disruption

Manufacturing production output fell in the month of September by 0.1% meaning that output is now 2.5% below February 2020 levels. Six out of 13 subsectors of manufacturing saw a decline in September 2021. Mostly impacted by supply chain challenges in the industrial sector.

Food manufacture and pharmaceuticals both saw growth in September from our comparison list however, automotive fell 8.2% as the sector is still being challenged as a result of the ongoing semi-conductor shortage, coupled with a decrease to the usual level of demand for new cars. This is exacerbated at the quarterly level where automotive experiences a worse Q on Q decline than others. With output falling 7.3%. By comparison aerospace manufacture output over the same period fell by 0.2% and in the month of September fell by a further 0.5%.

Aerospace output remains low and weak

Aerospace is the manufacturing sector that remains significantly weaker than in February 2020, at 38.2% smaller in terms of output. Aerospace manufacturing output had stabilised in recent months, albeit at low levels and the quarterly decline is relatively small.

From a services perspective, air transport continued to grow as COVID related travel restrictions eased, growing by 23.9% in September 2021, but remaining 73.3% below its pre-coronavirus pandemic level. This should provide some confidence for manufacturers that demand is on its way to return, but as anticipated the feed through to the manufacturer side, following a return of consumers, is lagged. UK flights (arrivals and departures) in September remained around 45% below 2019 levels, with expectations that further changes to travel testing requirements and the October half term would see improvements in the coming months.

The chart shows the low and flat output for the aerospace sector compared to other manufacturing industries and total UK GDP. More turbulent times in adjacent sectors in recent months are evident, but the prolonged low levels of output for aerospace will create long term distortions.